America Second, Neighbours First?

Issue 3;

Financials, Communications, and Industrials dominate the Leading/Emerging trends this week, but most interestingly, all of them are European or the Rest of the World. The US is not represented in the top leading or emerging trends, but is represented in over 90% of weakening trends. Apple, Eli Lilly, Chevron – tech, healthcare, and energy – are all weakening. The US relative weakness is broad.

The number of strong and emerging trends has decreased this week, but many remain bearish.

Weekly Insight

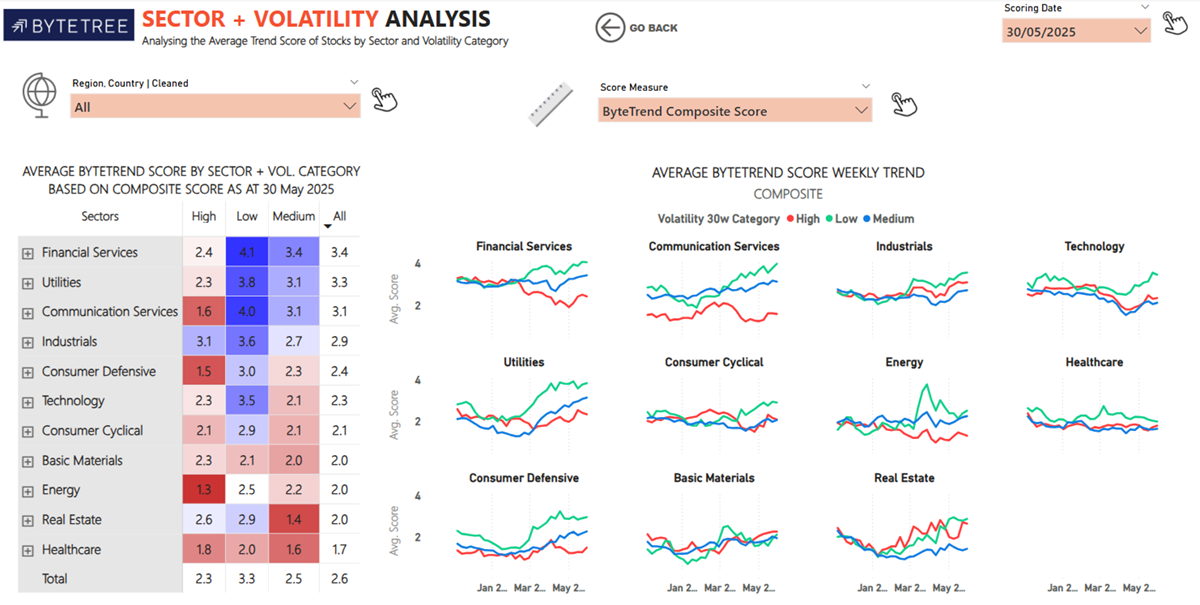

Today, we’d like to highlight this Sector + Volatility Analysis table.

Sector + Volatility Analysis

It shows the 30-week performance of each volatility category within each sector.

A few notable things stand out. Firstly, the significant strength of low volatility stocks. The strongest categories are low volatility financial services, utilities, communications and industrials. In financial services, the line chart shows clearly that medium vol stocks, the blue line, have performed roughly in line with the market, while low vol financials have outperformed and high vol ones have underperformed.

Even in technology, mid- and high vol have visibly underperformed, while low vol has again outperformed. Sectors are one thing, but this clearly shows the effect that company quality has in periods of change, like 2025 has been so far. In turbulent times, it pays to be stable. Volatility reflects investor confidence and business resilience. It is typically hard-won – investors need proof of a company’s stability before they trust it.

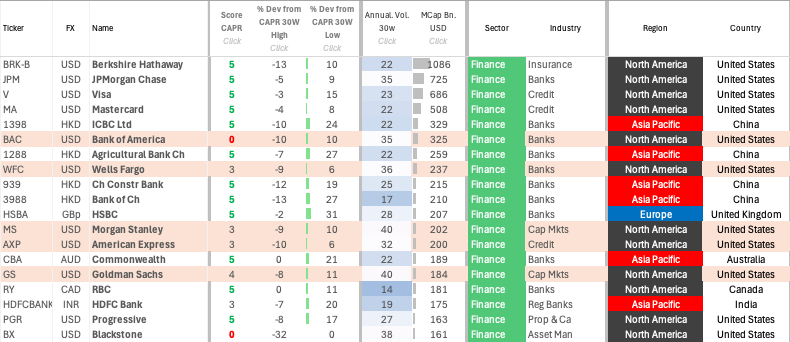

If you look at the world's top 20 financials, you can see this quite clearly. The first five companies not to have a CAPR score of 5 are all higher vol: BAC, WFC, MS, AXP, and GS. JP Morgan and Indian bank HDFC are notable exceptions.

Financials – Top 20

We are delighted to announce that the user guide for GTI: Premium is now published. You can find it here, and we hope it helps guide you through the spreadsheet. We hope to further improve the user guide based on your feedback – please write to us at gti@bytetree.com.