Energy is Back

Issue 20;

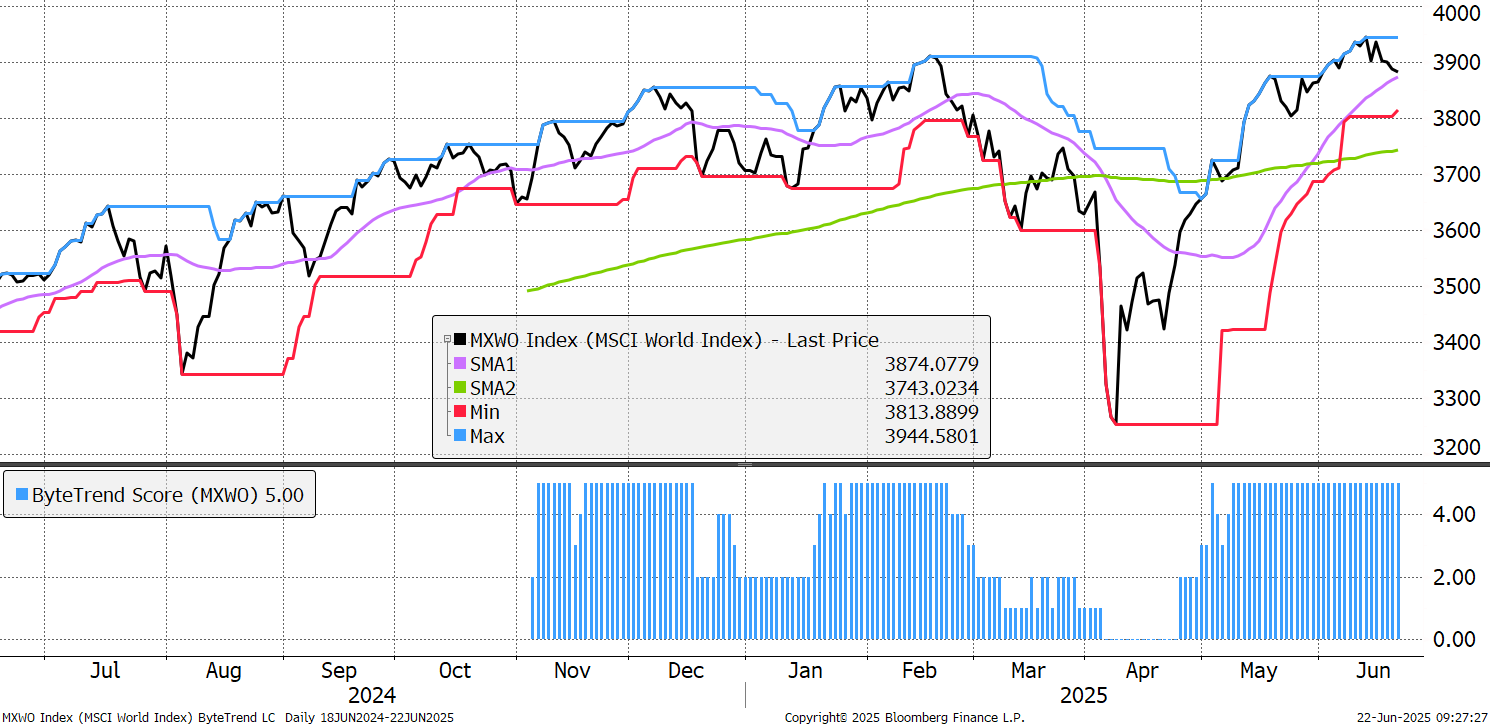

The World Index has eased back towards the 30-day moving average. The ByteTrend Score is still a 5, but it wouldn’t take much weakness to downgrade that. The market has had a strong rally, and a period of cooling should come as no surprise.

World Index – Developed Markets - Daily

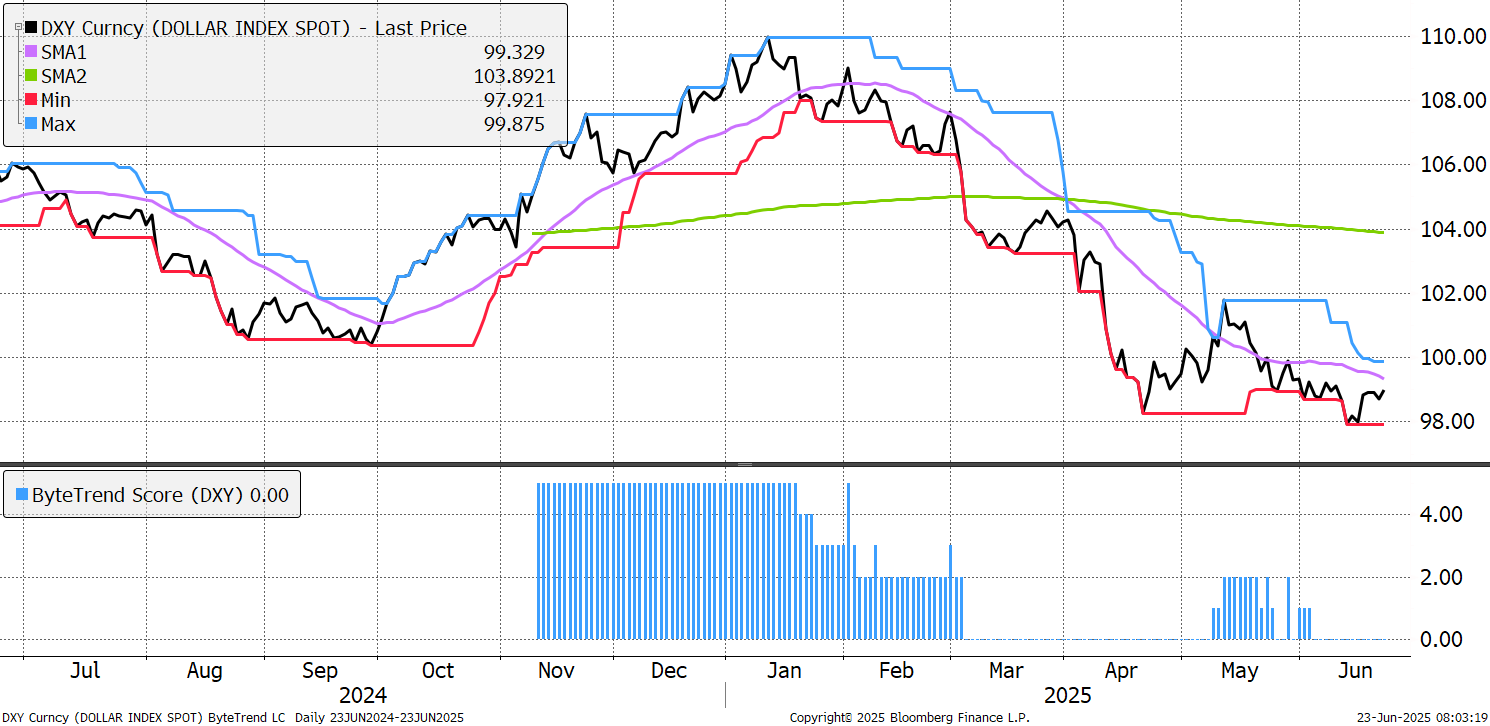

It could be that the dollar will rally following a period of weakness in 2025. Events in Iran have not led to a meaningful fall in US bond yields, as would normally be expected. Yet the dollar has risen slightly and could rally further. The ByteTrend Score is still 0, but it wouldn’t take much to move it higher as this year has seen large, long positions develop in EUR, GBP, JPY and others. Investors are now short the dollar, and a counter-trend rally remains a risk for stockmarkets.

Dollar Index - Daily

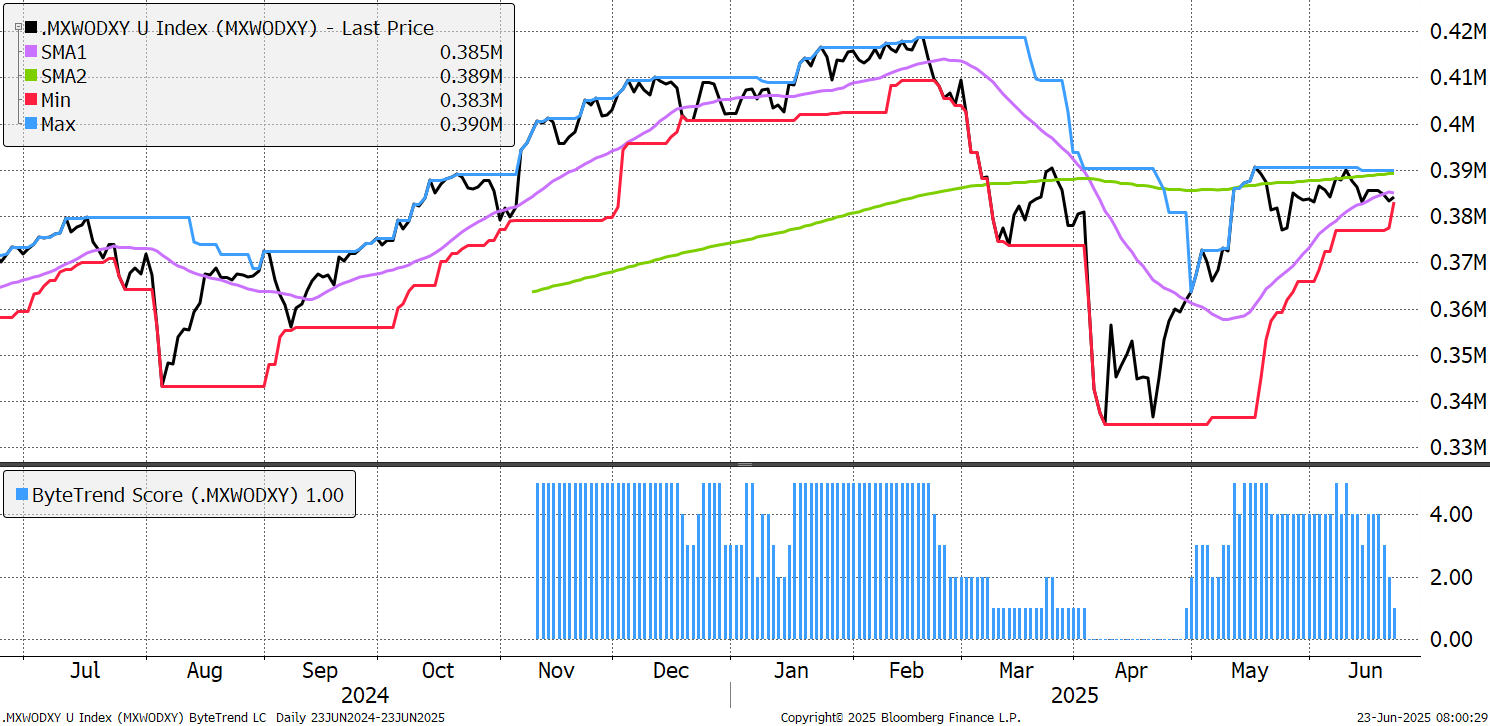

Looking at the World Index in non-dollars terms (viewed in a FX basket), the ByteTrend Score drops to a 1. On this basis, the World Index never made a new high and could be rolling over.

World Index – Developed Markets – Daily in non-US dollars

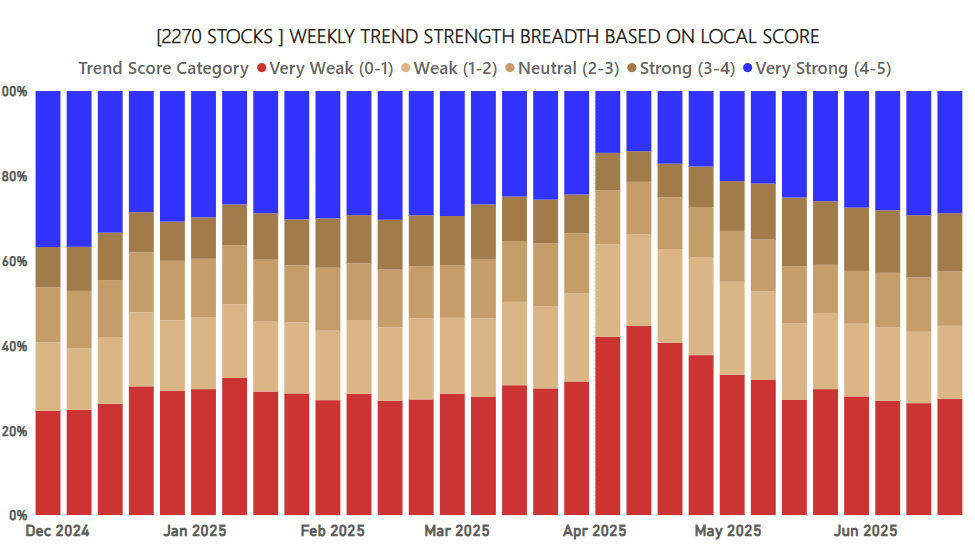

There is a modest deterioration in market breadth since last week. The weak trends (red) have risen slightly.

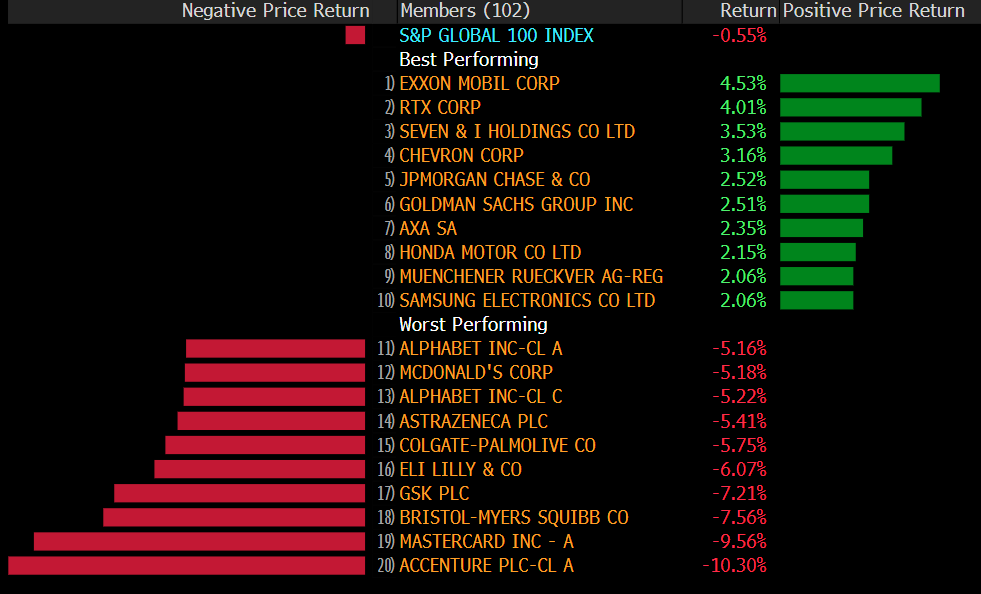

Leaders and Laggards

Oil stocks led the markets last week as seen by Exxon and Chevron in the World Top 100 Index.

Brent Crude USD

Banks and insurance also feature which has been a steady theme this year.

The loser list is more telling. Accenture was the weakest performer, which was flagged last week on the GTI-200 Bear list. Mastercard shows up too, which is often seen as a proxy for economic growth. Several quality stocks also show such as Colgate, and McDonalds, but the greatest show comes from pharmaceuticals, which has consistently shown weakness in recent issues.

Developed Markets Leaders and Laggards

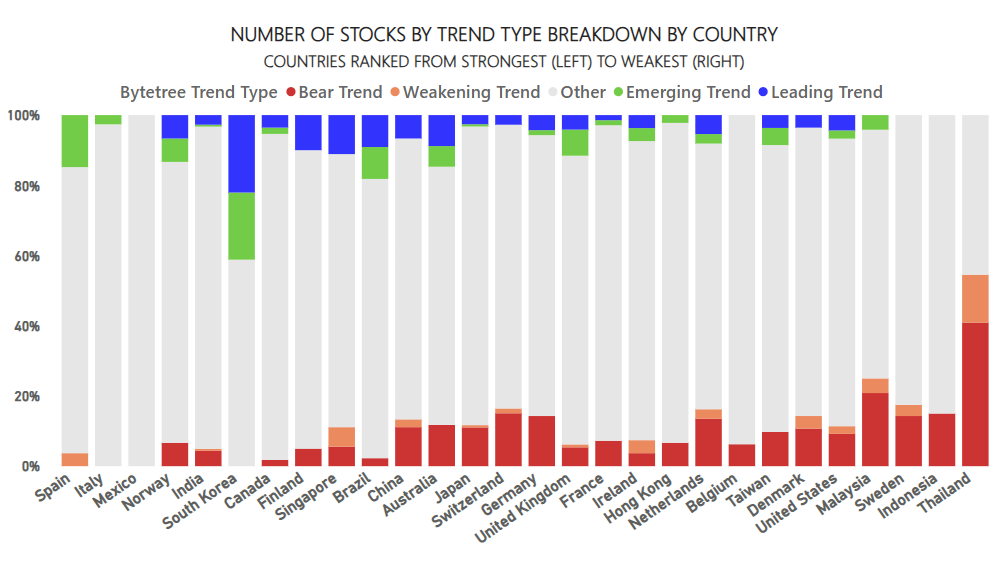

The GTI Premium spreadsheet keeps evolving and has become a powerful source of market intelligence. This latest chart shows the number of stocks for each country, by trend signal. This week, South Korea has many leading and emerging trends, but no bear trends. Brazil is also strong.

In contrast, Thailand, has no bull trends and many bear trends. Political events, and a leaked phone call by the pm, have seen the risk of a military coup rise. It is notable that Indonesia analysis also show weakness.

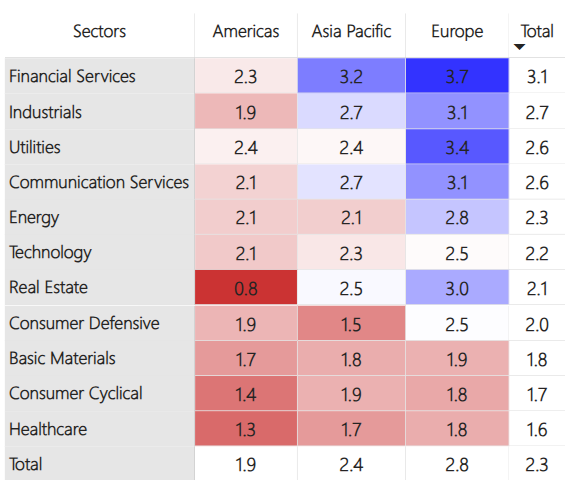

The heatmap still sees the leading group to be European financials followed by utilities. European real estate has also improved since last week. Basic materials, consumer cyclicals and healthcare remain weak with US real estate the stand out weakest global stock group.

Average ByteTrend Score by Region and Sector Heatmap - CAPR

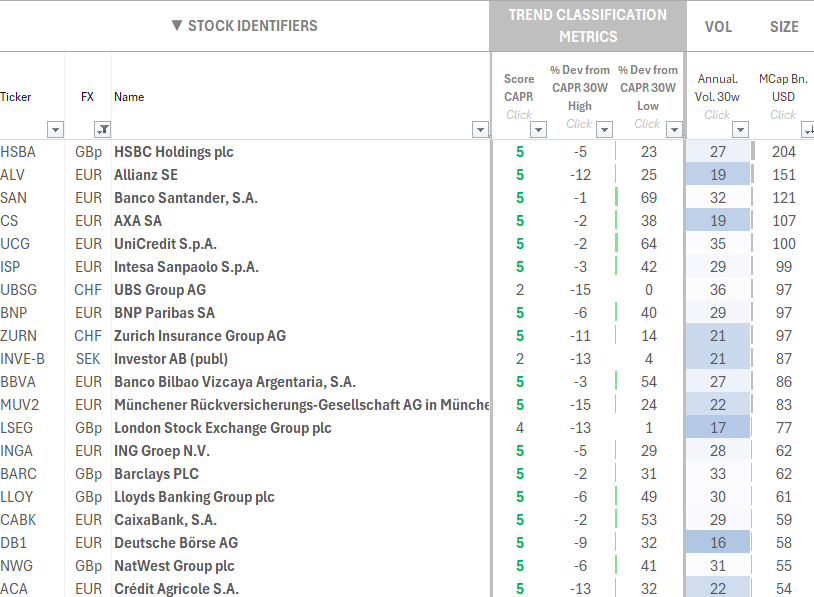

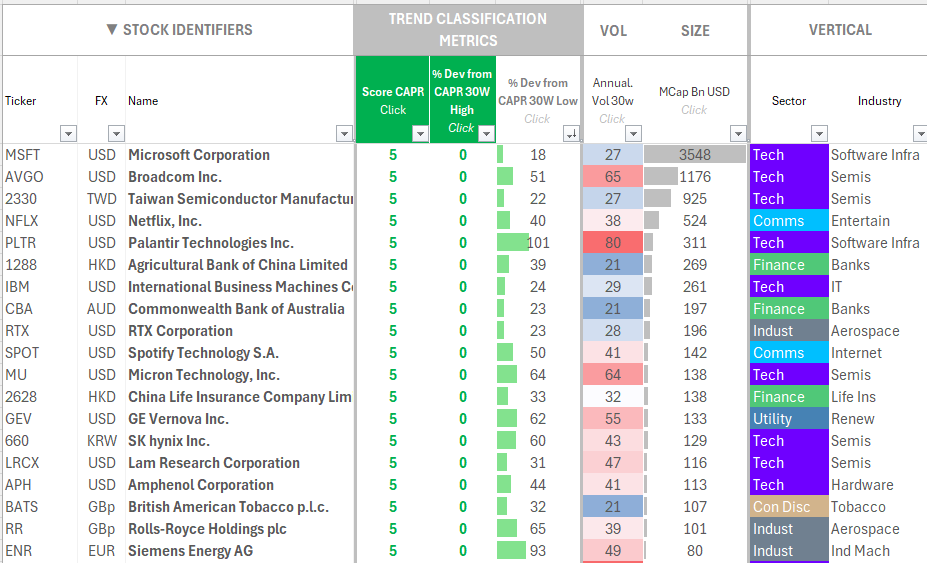

The GTI Premium spreadsheets includes all 2,500+ stock in the global universe. They can be sorted for many different things. These are European Financials, with the top 20 (by market cap) shown.

Strongest – European Financials

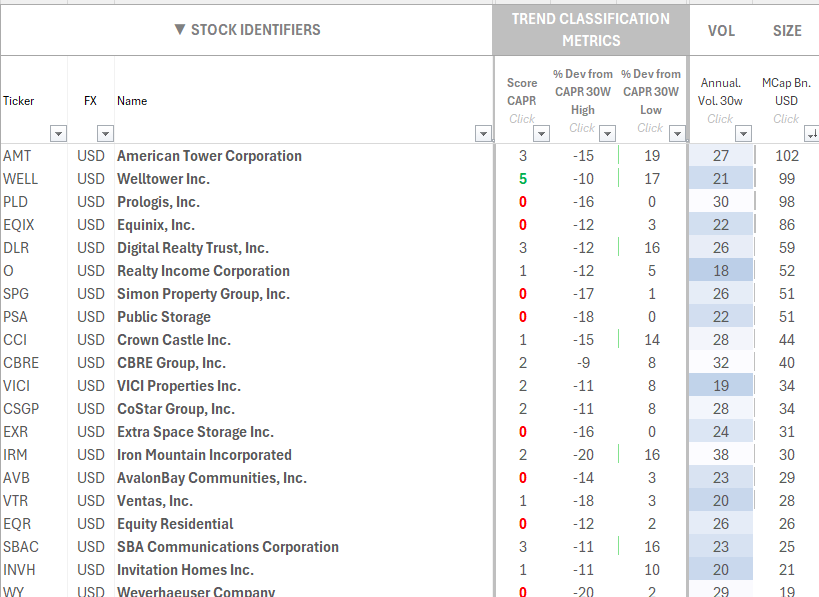

This list shows the top 20 US Real Estate stocks.

The weakest - US real estate

This week sees consistency in the trend groups.

Leading Trends with New Highs

These stocks are trading at the 30-week CAPR highs with a ByteTrend Score of 5. All charts shown are CAPR rebased to 100.

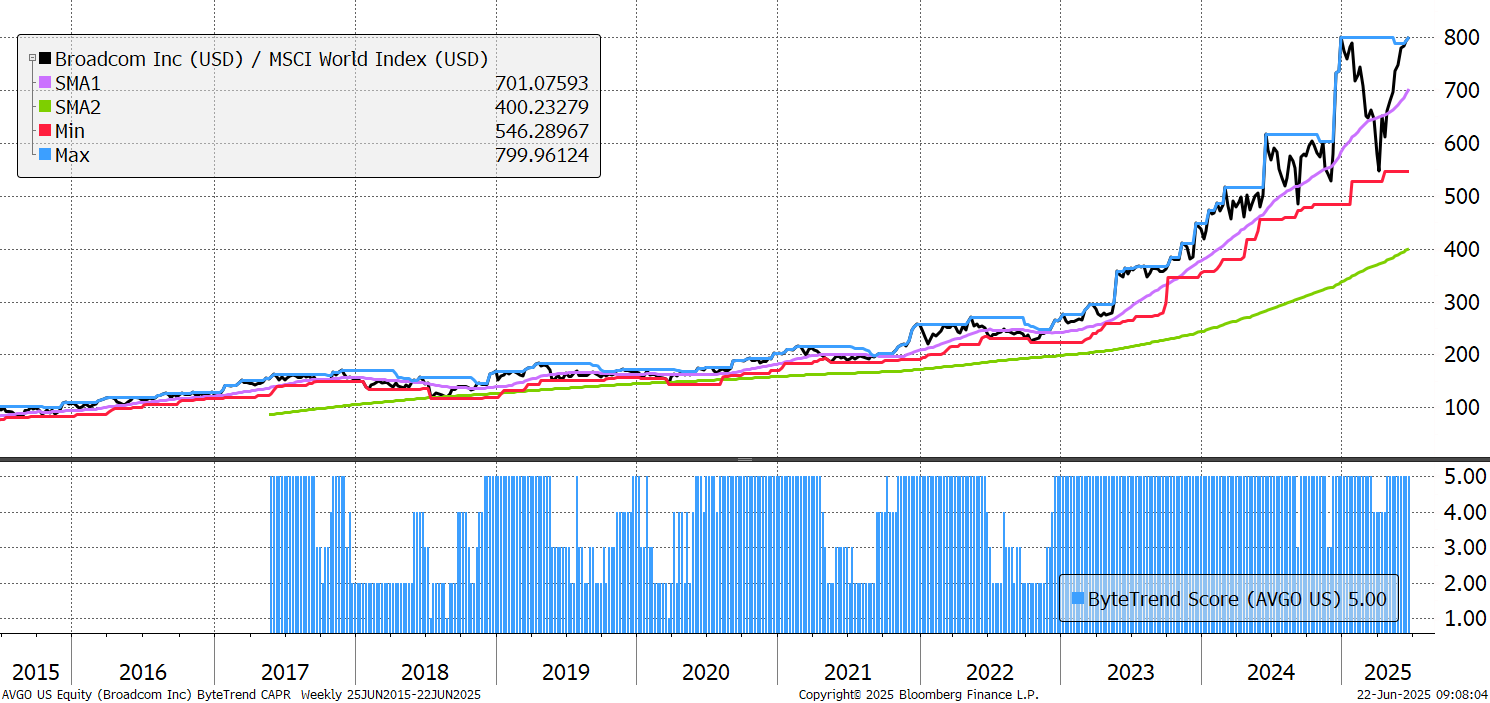

Broadcom looked like a bubble that was bursting just a couple of months ago, but here we are again at new CAPR highs and a score of 5. Its custom AI chips for hyperscalers made it a winner in the data centre boom, and high margins and recurring revenues help too. Revenue growth has just slowed in the last two quarters though, and the EV/Sales is over 20x, so there is little room for further disappointment.

Broadcom

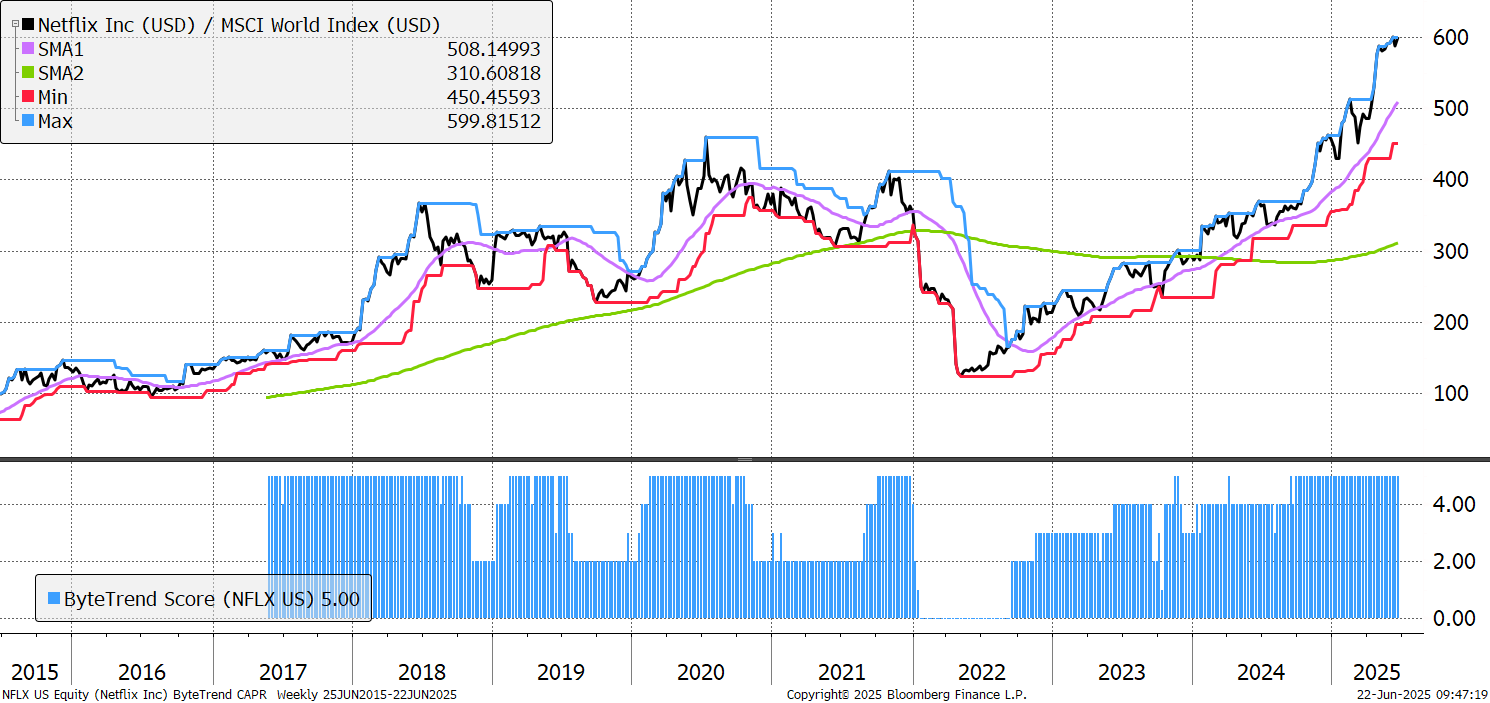

Netflix wins a gold star. The pandemic and tariff troubles were the major incidents in the last few years, but Netflix seemed to benefit from both. Crackdowns on password sharing, a growing base of proprietary content, new deals with traditional television stations in France - it just goes from strength to strength. Market leadership wasn’t always certain, but it’s here now and valuations reflect that with EV/Sales at 13x.

Netflix

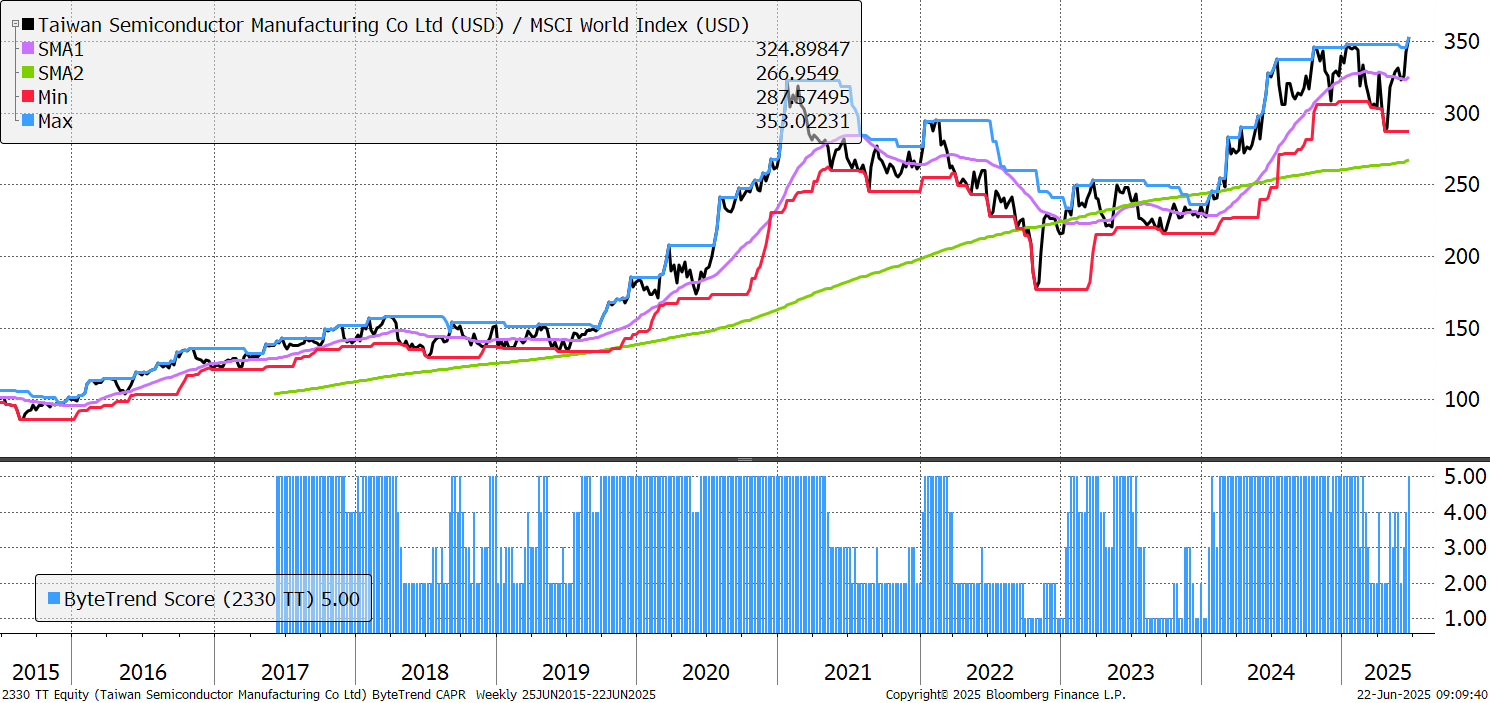

Taiwan has been at the top of the list for expected geopolitical strife, but the trouble has come elsewhere. April's tariff blip is forgotten (for now) and TSMC is investing heavily in American chip fabrication plants with over $100bn in capex. Its largest factory, Fab 18, measures 10 million square feet, and Buffett is a long-term investor. It dominates what many think is the most important market in the world and stays relentlessly ahead of its peers.

TSMC

IBM was long mocked for its failure to keep up, as it slowly sunk lower relative to the world index. However, a turnaround has come through a strategic pivot to what they call “hybrid” cloud (mixing public and private cloud services) and AI businesses, anchored by the $34bn acquisition of hybrid cloud software business Red Hat in 2018/19, and divestiture of legacy businesses. This shift has led to accelerating revenue growth and improved margins, restoring investor confidence. Revenue per employee fell for 25 years but since 2020, has risen each year.

IBM

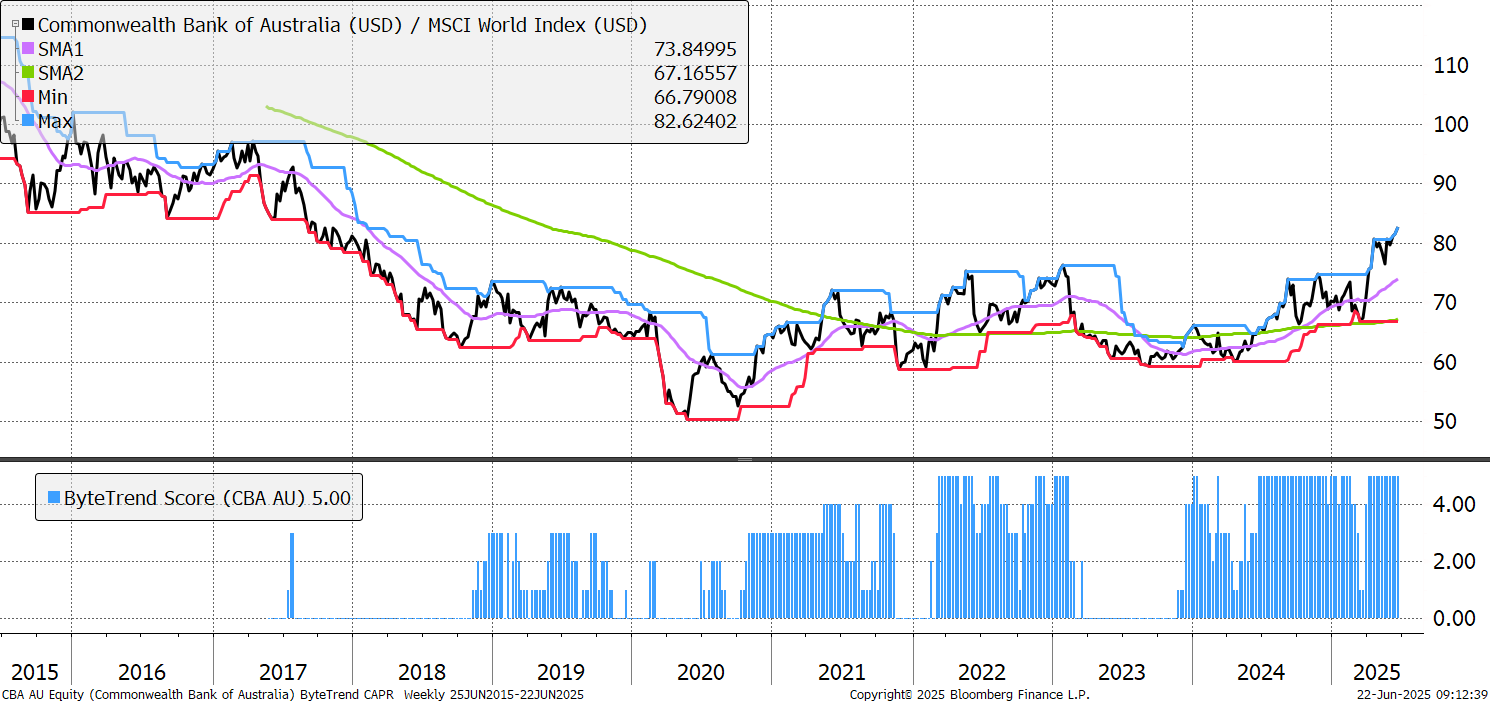

Financials like the Commonwealth Bank of Australia (CommBank) continue to do well all over the world – Canada, Australia, China and more all appear from outside Europe. CommBank was Australia’s first to be backed by government guarantee and funded much of their war effort in WW2. More recently, it was the first to offer online banking in Australia and has gained a reputation for technological leadership. Book value/share dipped after covid but started to pick up again in late-2023, and the share price has followed suit.

CommBank

With over 4 trillion yuan in assets, China Life Insurance Co is the largest in China by market share and one of the world’s biggest insurers. It’s not a common name in the west but is one of China’s biggest brands. It has a huge agency sales force, and a broad product portfolio, especially in health and retirement products. Despite steady growth in book value/share, it has suffered a very long decline, and this is its first score of 5 in at least a decade. New regulatory directives will be pushing it to invest in more Chinese equities.

China Life Insurance Co

There are 88 additional leading trends with new highs in the GTI Premium universe. There are several banks and insurance companies in Europe and more importantly, Asia. Industrials and defence stocks feature, as does AI enablement. UK energy stock, Ithaca also shows up as new licences are expected in the North Sea.

Emerging Trends

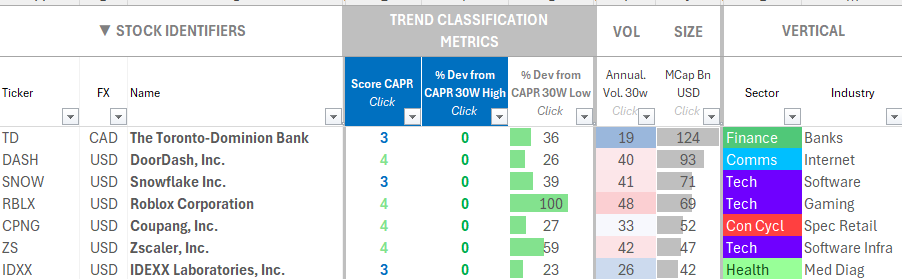

These stocks are trading at the 30-week CAPR highs with a ByteTrend Score of less than 5. They don’t have to be in an uptrend, just emerging. All charts shown are CAPR rebased to 100.

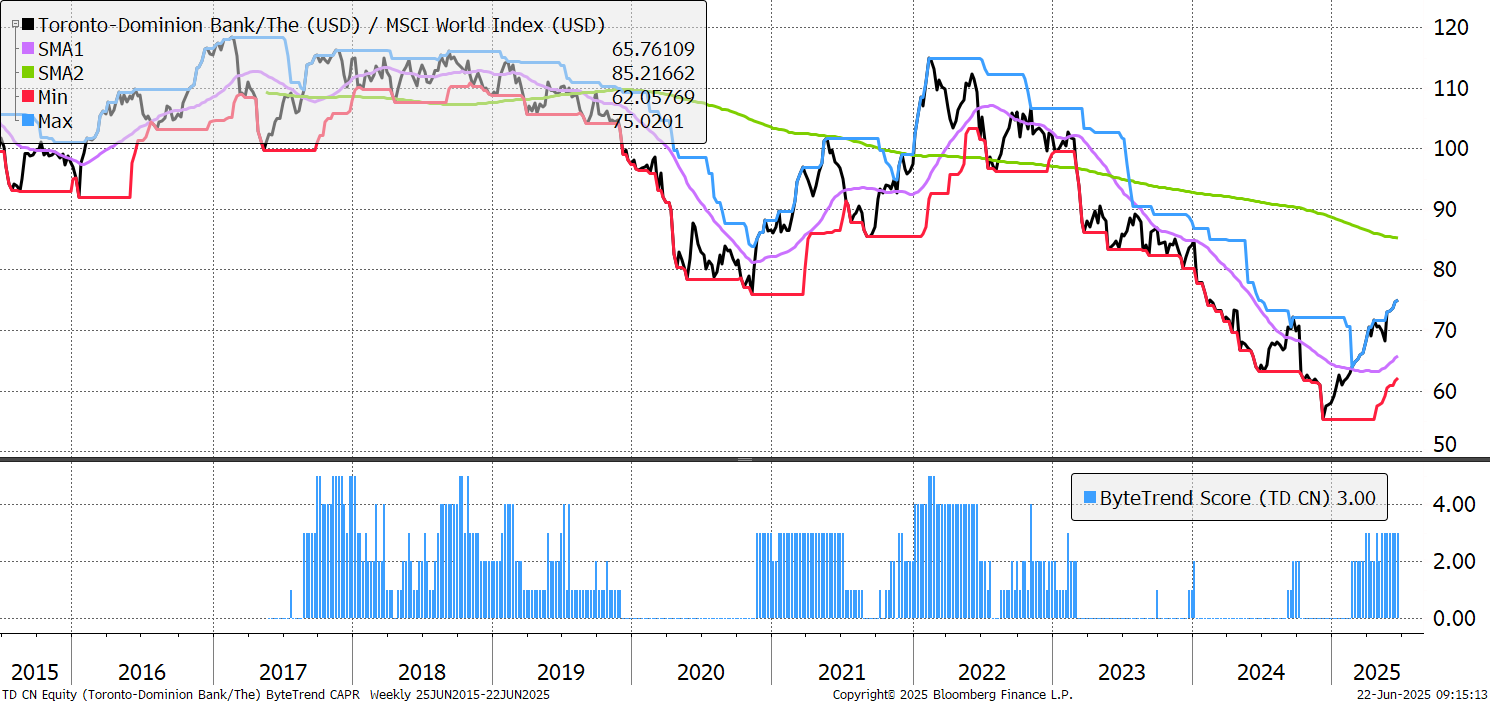

TD Bank appears again, as the Canadian financial strength continues. This led to a recommendation in The Multi Asset Investor of a Canadian ETF, as part of its absolute return mandate. TD Bank’s windfall from the sale of Charles Schwab stake is initially being used to fund share buybacks, with 6% of the shares being bought back in the last two years. It trades on 1.4x book value, nearly the lowest since 2008, and the underlying business in growing healthily, so management have good reason to view their shares as undervalued. Given Schwab trades on 4.0x book, it looks like a sensible move by management.

TD Bank

Snowflake’s infamous IPO came at the peak of the post-pandemic bubble, and it has been duly punished. However, raising capital at the top is smart work, as you get more for less – it’s management’s way of selling high. Its EV/Sales has calmed down from around 200x (!!) then to 18x today, as it shows signs of recovery. Growth has slowed in the last few years but remains high at 27% YoY. It wasn’t a bad business, just a high price, and it’s still hard to call it cheap.

Snowflake